The dawn of 2026 has ushered in a period of profound transformation for the United States residential renewable energy market, characterized by a fundamental decoupling of consumer demand from direct federal support. For nearly two decades, the American homeowner enjoyed a relatively straightforward financial relationship with the federal government regarding solar energy adoption. The mechanism of this support was the Section 25D Residential Clean Energy Credit, a statutory provision that allowed individual taxpayers to claim a substantial percentage of their solar system’s cost—historically 30%—as a direct credit against their personal income tax liability. This era, defined by the simplicity of "buy, install, claim," has officially concluded. As of January 1, 2026, the statutory authority for Section 25D has expired for new residential solar electric property placed in service, pursuant to the phase-out schedules codified in the legislation widely referred to as the "One Big Beautiful Bill Act" (OBBBA)1.

The expiration of Section 25D was not an accidental sunset but a deliberate legislative choice to pivot federal fiscal support away from broad consumer subsidies and toward targeted commercial deployment and domestic manufacturing security. The legislative text of the OBBBA, signed into law on July 4, 2025, repealed the residential credit for expenditures made after December 31, 2025, leaving millions of potential solar adopters facing a stark economic reality: the gross cost of a solar installation is now the net cost, representing an immediate 30% to 40% price increase for direct purchasers compared to the previous year3.

However, the demand for distributed energy generation has not abated. Rising utility rates, grid instability, and the increasing electrification of the home (via heat pumps and electric vehicles) continue to drive homeowner interest in solar photovoltaic (PV) systems. Furthermore, the federal government’s support for clean energy has not evaporated entirely; rather, it has shifted venues, moving from the individual tax return (Form 5695) to the corporate tax return (Form 3468). We are currently witnessing a massive structural migration from residential ownership models to third-party ownership (TPO) models. This shift is driven by the continued availability—and even enhancement—of the Section 48E Clean Electricity Investment Tax Credit (ITC), which remains available to commercial entities2.

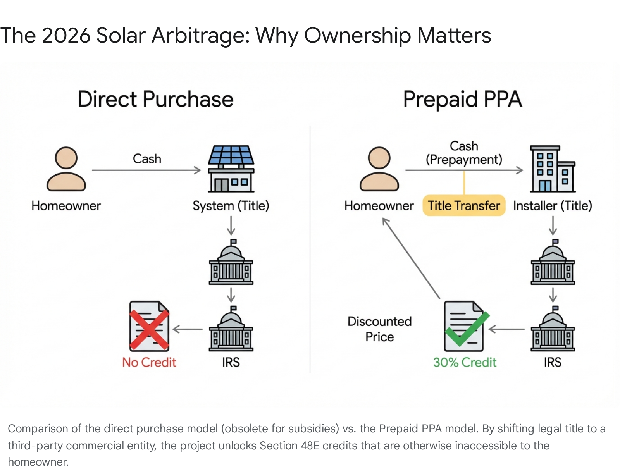

The current market environment is defined by regulatory arbitrage. The disparity between the expired residential credit and the active commercial credit has birthed a new class of financial products designed to bridge the affordability gap. Chief among these is the "Prepaid Power Purchase Agreement (PPA)" or "Prepaid Lease," a mechanism that allows homeowners to indirectly access the 30% federal subsidy by transferring legal ownership of the system to a commercial entity—the installer or a specialized financier—for a mandatory tax compliance period6. While these structures offer a lifeline for solar affordability, they introduce complex legal, financial, and regulatory risks that were virtually nonexistent under the direct ownership model.

1.1 The Statutory Cliff: Section 25D vs. Section 48E

To navigate the 2026 solar market, one must first comprehend the precise nature of the "subsidy cliff." For years, the distinction between residential and commercial solar was primarily one of scale and interconnection complexity. In 2026, it is a fundamental distinction of subsidizability based on the tax identity of the system owner.

Section 25D, the now-defunct residential credit, was unique in its accessibility. It required only that the taxpayer reside in the home where the improvements were made and that the property be used as a residence8. It did not require the taxpayer to be a business, nor did it involve complex depreciation schedules. Its expiration creates a vacuum that the market is scrambling to fill.

In stark contrast, Section 48E, the "Clean Electricity Investment Tax Credit," remains a pillar of federal energy policy. Enacted as part of the Inflation Reduction Act and modified by the OBBBA, Section 48E provides a base credit of 30% for qualified facilities that generate electricity with a greenhouse gas emissions rate of zero9. Crucially, this credit is available to "taxpayers," which in the context of the Internal Revenue Code generally refers to business entities capable of claiming the Investment Tax Credit (ITC) and capitalizing the asset for depreciation purposes.

The arbitrage opportunity arises from the fact that the physical asset—the solar panel—is identical in both scenarios. A solar panel bolted to a roof owned by a homeowner generates $0 in federal credits because the homeowner is an ineligible entity under the expired Section 25D. However, the exact same panel on the exact same roof, if legal title is held by a commercial corporation (the installer or a third-party financier), generates a tax credit equal to 30% of the cost basis under Section 48E5. This creates a powerful economic incentive to sever the link between "home ownership" and "solar system ownership."

1.2 The Rise of the "Shadow Owner"

This regulatory landscape has necessitated the resurrection and mutation of the Third-Party Ownership (TPO) model. Historically, TPO models like leases and PPAs were used primarily to overcome the barrier of high upfront costs, allowing homeowners to pay $0 down in exchange for monthly payments. In 2026, the primary function of TPO is not financing, but tax credit monetization.

The "Prepaid PPA" described in your query represents the evolution of this model for a cash-rich or financing-capable homeowner who would have preferred to buy the system outright. In this arrangement, the homeowner pays the full "purchase" price upfront—often 70% of the gross system value—but signs a contract designated as a "Power Purchase Agreement" or "Lease" rather than a "Sales Contract."

By retaining legal title to the equipment, the installer qualifies as the "taxpayer" for Section 48E purposes. They claim the 30% ITC and, theoretically, pass the value of that credit through to the homeowner in the form of a lower upfront price. The homeowner effectively buys a 20-year service contract rather than a physical asset, with the installer acting as a "shadow owner" solely to satisfy IRS requirements6.

1.3 The OBBBA’s Leasing "Carve-Out" Confusion

A critical point of confusion for homeowners in 2026 stems from the specific text of the OBBBA regarding leasing restrictions. In the legislative chaos preceding the bill's passage, early drafts proposed a blanket prohibition on claiming tax credits for any residential renewable energy property that was leased to a third party. Such a provision would have effectively destroyed the residential TPO market, rendering the Prepaid PPA model illegal11.

However, refined legal analysis of the enacted statute reveals a significant carve-out. The final statutory language significantly narrowed this restriction. The prohibition on claiming commercial credits for leased residential property applies only to solar water heating property and small wind energy property12. The legislative intent appears to have been to curb specific abuses in those niche markets rather than to dismantle the rooftop solar industry.

Crucial Insight: Residential solar photovoltaic (PV) systems—the panels that generate electricity—were explicitly exempted from this ban. Therefore, the "Prepaid PPA" for solar electric systems remains a legally viable path to access Section 48E credits in 2026. Homeowners should not be deterred by outdated news reports or misinterpreted headlines citing a "leasing ban" unless they are installing wind turbines or solar thermal water heaters. This distinction is vital: if a homeowner is considering a hybrid system (e.g., solar PV plus a small wind turbine), the financing structure may need to be bifurcated, as the wind portion would be ineligible for the lease-based credit while the solar portion would qualify14.

1.4 The "Technology Neutral" Shift and Phase-Out

The transition to Section 48E also introduces a "technology neutral" framework. Unlike previous credits that picked winners (e.g., solar vs. wind), Section 48E applies to any facility with zero greenhouse gas emissions. This broadens the scope of eligible technologies but ties their longevity to national emissions targets. The OBBBA mandates that these credits will phase out once the U.S. electricity sector achieves a 75% reduction in greenhouse gas emissions from 2022 levels, or by 2032, whichever is later9.

While 2026 is well before this phase-out horizon, the legislative volatility underscores the temporary nature of these incentives. The "Prepaid PPA" is likely a transitional instrument, a bridge solution engineered to navigate the specific tax code environment of the mid-to-late 2020s.

Part II: Anatomy of the "Prepaid PPA" – Mechanics of the Loophole

The "5-year PPA with a $1 buyout" is not a simple purchase agreement; it is a sophisticated financial derivative designed to separate the tax attributes of the solar system from the use attributes. For the homeowner accustomed to simple retail transactions, this structure can appear opaque. Understanding the mechanics is essential for assessing the legitimacy of any offer and distinguishing between a clever financial product and a fraudulent tax scheme.

2.1 The Financial Structure: Following the Money

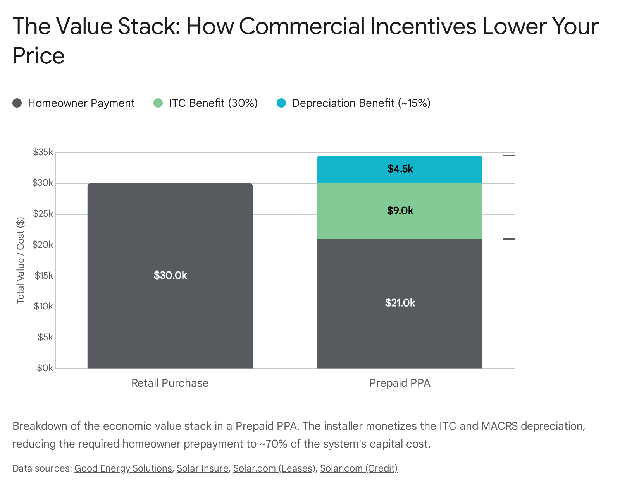

In a standard purchase scenario prior to 2026, the transaction flow was linear: the homeowner paid the gross system cost (e.g., $30,000), received title to the system, and subsequently claimed a $9,000 credit on their next tax return. The net cost was $21,000.

In the 2026 Prepaid PPA model, the transaction is bifurcated to optimize tax outcomes:

- The Prepayment: The homeowner pays the installer a lump sum upfront. This payment is legally characterized not as a purchase price for equipment, but as a prepayment for all the electricity the system is expected to generate over the initial contract term (typically 20-25 years).

- The "Discount": Because the installer (as the legal owner) will claim the 30% ITC, they discount the prepayment amount. If the system cost is $30,000, they might charge the homeowner $22,000 upfront. This effectively passes through the majority of the subsidy value to the consumer, lowering the barrier to entry6.

- Title Retention: The installer retains legal title to the equipment. This is a non-negotiable requirement. If the homeowner holds the title, the commercial credit eligibility vanishes, as the property would be considered "personal use property" under the tax code.

- The "Recapture Period": The Internal Revenue Code mandates that the investment tax credit vests over a five-year period under Section 50(a). If the owner (the installer) disposes of the system—by selling it to the homeowner, for example—before this five-year period concludes, a portion of the tax credit is "recaptured" (clawed back) by the IRS.

- Year 1: 100% recapture risk

- Year 2: 80% recapture risk

- Year 3: 60% recapture risk

- Year 4: 40% recapture risk

- Year 5: 20% recapture risk

- Year 6 (Day 1): 0% recapture risk2.

Insight: This statutory vesting schedule is the primary reason why these contracts are structured as "5-year" or "6-year" agreements regarding the transfer of ownership. The installer cannot transfer ownership to the homeowner earlier without suffering a severe financial penalty, which they would invariably pass on to the consumer in the form of higher costs or termination fees.

2.2 The "Put" and "Call" Options

The transition from the PPA structure to full homeownership usually occurs via specific options written into the contract. These options are the legal mechanisms that facilitate the eventual transfer of title once the tax credit recapture period has expired.

- Call Option: The homeowner has the right (but not the obligation) to purchase the system at the end of year 6. This allows the homeowner to take control of the asset if they choose.

- Put Option: The installer has the right to force the homeowner to purchase the system (usually for a nominal fee or Fair Market Value) at the end of year 6.

This interplay of options is where the "$1 buyout" marketing claim originates. Installers want to assure homeowners that this arrangement is "basically ownership" with a delayed title transfer. However, as will be explored in Part III, a guaranteed $1 buyout is a massive red flag that can trigger IRS audits by signaling that the transaction was never a genuine lease15.

2.3 Depreciation Benefits (MACRS)

Beyond the 30% ITC, commercial owners can depreciate the solar asset using the Modified Accelerated Cost Recovery System (MACRS). In 2026, depending on the specific tax appetite of the installer or their financing partners, they may be able to write off a significant portion of the system's value—often 100% in the first year under Bonus Depreciation rules, provided they meet certain criteria5.

This depreciation benefit is worth an additional 10-15% of the system cost in cash-equivalent terms to a profitable corporation. In a competitive market, a portion of this benefit should also be passed through to the homeowner, further lowering the prepaid price.

Consumer Tip: When evaluating a Prepaid PPA quote, a sophisticated homeowner should ask specifically: "How much of the MACRS depreciation benefit is being passed through to me in the prepaid price?" If the installer claims they cannot monetize depreciation or refuses to acknowledge its value, they are likely padding their margins or lack sophisticated tax equity partners, which results in a higher effective cost for the homeowner17.

2.4 The Impact of Interest Rates on Prepayment

The viability of the Prepaid PPA model is also sensitive to the broader interest rate environment of 2026. Because the homeowner is prepaying for 20-25 years of power, they are effectively locking up capital. If interest rates are high, the "opportunity cost" of that capital is significant. Installers may market the prepaid option as a way to avoid high interest rates on solar loans, which might hover around 9-11% for unsecured consumer credit. By shifting the financing burden to the homeowner's cash reserves (or a lower-interest Home Equity Line of Credit), the Prepaid PPA can offer better long-term economics than a traditional loan, even before accounting for the tax benefits.

Part III: The "Disguised Sale" Trap – Legal Risks of the $1 Buyout

The single most dangerous element of the 2026 Prepaid PPA market is the marketing promise of a "$1 transfer" or "automatic ownership" after 5 years. While highly effective for closing sales with hesitant homeowners, this structure risks violating IRS Section 707 provisions on "Disguised Sales," potentially invalidating the tax credits that underpin the entire financial logic of the deal.

3.1 The IRS View: Lease vs. Sale

The Internal Revenue Service is acutely aware of schemes designed to recharacterize sales as leases to shift tax benefits. Under Section 707(a)(2)(B), the IRS scrutinizes these transactions to determine if they are "true leases" (or valid service contracts) or merely financing arrangements for a sale18.

- True Lease/PPA: In a valid lease, the lessor (installer) retains the risks and rewards of ownership. The lessee (homeowner) is merely paying for the use of the asset (or the power it generates). Crucially, the lessor must have a meaningful "residual interest" in the property at the end of the term.

- Disguised Sale: If the terms of the agreement are structured such that the homeowner is effectively the owner from Day 1—bearing all risks, enjoying all rewards, and guaranteed title transfer—the IRS views the "lease" as a sham. The transaction is recharacterized as a sale that occurred at the inception of the contract16.

If the IRS successfully recharacterizes a Prepaid PPA as a Disguised Sale, the consequences are catastrophic for the deal economics:

- Denial of ITC: The IRS disallows the Section 48E credit because the "taxpayer" (the installer) did not retain true tax ownership of the asset.

- ITC Recapture: The installer is assessed a bill for the full value of the 30% credit, plus interest and significant penalties for underpayment of tax.

- The Clawback: Most PPA contracts contain indemnification clauses buried in the fine print. These clauses often stipulate that if the installer loses the tax credit due to a regulatory determination or change in law, the customer (homeowner) must make them whole. In this scenario, the homeowner could suddenly be liable for the $9,000+ that was supposedly "saved" via the prepaid discount15.

3.2 The "Fair Market Value" (FMV) Requirement

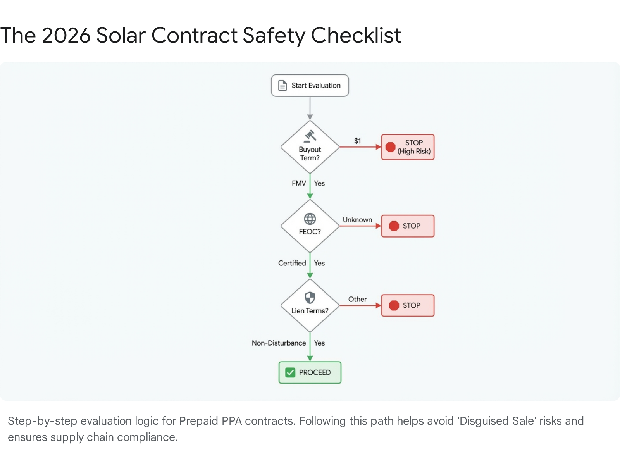

To satisfy the IRS that a transaction is a True Lease and avoid the disguised sale trap, the buyout option at the end of the term must be at Fair Market Value (FMV), not a nominal fixed price like $121.

- The Problem with $1: A $1 purchase option implies that the installer has no intention of retaining the asset and that the equity has already implicitly transferred to the homeowner. It creates a "compulsion to exercise" the option, which is a hallmark of a conditional sale in the eyes of tax courts15.

- The FMV Solution: Legitimate, tax-compliant contracts will state: "At the end of Year 6, the customer may purchase the system for the GREATER of Fair Market Value (as determined by an independent appraiser) or a scheduled minimum value."

The Conflict: Homeowners inherently dislike FMV clauses because they create financial uncertainty. "What if the system is still worth $15,000 in 6 years? I have to pay that again?" This fear is a major friction point in sales.

Installers often attempt to assuage this fear by arguing that a 6-year-old system, technically "used" and bolted to a specific roof (making removal and re-installation costs exceed resale value), has a very low FMV—perhaps even zero. While economically plausible, writing "$1" into the contract removes the necessary uncertainty that validates the lease structure.

Insight: While the actual FMV might be low, the contractual right to buy it for $1 is legally perilous. A safer contract structure might specify a fixed percentage (e.g., 15-20% of original cost) or explicitly mandate an appraisal process. Homeowners should be extremely wary of contracts that guarantee a transfer for $0 or $1, as these are low-hanging fruit for IRS auditors.

3.3 The "Service Contract" Defense (Section 7701(e))

Some installers structure these deals not as leases but as "Service Contracts" to avoid the strict "True Lease" tests. Under IRS Section 7701(e), a contract is treated as a service contract rather than a lease if it meets certain criteria, such as:

- The service provider (installer) creates the property.

- The provider physically operates the property.

- The provider bears the risk of diminished receipts or increased costs23.

However, in a Prepaid PPA where the homeowner pays 100% of the cost upfront, the provider bears no risk of "diminished receipts"—they have already collected all their revenue. This lack of ongoing economic risk weakens the Service Contract defense and pushes the arrangement back toward the definition of a Disguised Sale. Sophisticated installers may retain some operational risk (e.g., performance guarantees) to bolster this defense, but the fundamental tension remains.

Part IV: The "One Big Beautiful Bill" (OBBBA) & Regulatory Landmines

The OBBBA did not merely end the residential credit; it introduced a complex new regulatory regime involving supply chain controls and strict deadlines. These provisions act as potential "landmines" for the unwary homeowner in 2026, creating scenarios where a project might fail to qualify for credits even if the ownership structure is sound.

4.1 Foreign Entity of Concern (FEOC) Restrictions

Starting in 2026, the OBBBA imposes strict supply chain controls on clean energy projects. Section 48E credits are disallowed if the project includes "material assistance" from or incorporates components manufactured by a "Foreign Entity of Concern" (FEOC). This definition primarily targets entities owned or controlled by the governments of China, Russia, North Korea, and Iran24.

- The Supply Chain Risk: The solar industry has historically been heavily reliant on Chinese supply chains for polysilicon, wafers, and cells. While many manufacturers have diversified to Southeast Asia, the OBBBA's "material assistance" rules are far-reaching. If an installer uses older inventory or non-compliant brands to cut costs, the system may generate zero tax credit.

- The Consequence: If the credit is denied due to an FEOC violation, the installer’s pricing model collapses. If the PPA contract has a "Tax Credit Eligibility Adjustment" clause (a common feature in commercial PPAs), the installer may have the legal right to bill the homeowner for the lost 30% credit value.

- Mitigation: Homeowners must demand a "Compliance Certificate" or similar warranty stating that the specific modules (panels) and inverters installed are FEOC-compliant for the 2026 tax year. Brands with established U.S. or allied-nation manufacturing footprints (e.g., Qcells, First Solar, REC) are generally safer bets than generic imports with opaque supply chains26.

4.2 The "Safe Harbor" Cliff: July 4, 2026

The commercial credits for solar are on a statutory phase-out trajectory related to construction start dates. For projects to qualify for the current 48E regime without being subject to stricter emission-reduction phase-outs or lower credit rates, they must "begin construction" by July 4, 20265.

- The 5% Safe Harbor Rule: Previously, installers could "safe harbor" projects by spending 5% of costs upfront, locking in tax credit eligibility for years. The OBBBA and IRS Notice 2025-42 have restricted this practice. The 5% safe harbor is now generally eliminated for large projects but is explicitly preserved for "Low Output Solar Facilities" (under 1.5 MW)29.

- Impact on Homeowners: Since residential systems are well under the 1.5 MW threshold, installers can use the 5% safe harbor to lock in 2026 credit rules for installations that might physically occur in late 2026 or 2027. However, this requires the installer to be highly organized with their procurement and documentation. Disorganized installers may miss this deadline, jeopardizing the credit availability for projects installed in the second half of the year.

Consumer Warning: Be cautious of installers rushing to sign contracts in June 2026 with promises of "locking in" the credit. Ensure they have the inventory and documentation to actually meet the safe harbor requirements before the July 4 deadline.

4.3 The "Domestic Content" Bonus: A Hidden Negotiating Chip

In 2026, the Section 48E credit has a base rate of 30%. However, if the project meets specific "Domestic Content" requirements (100% US steel/iron and a minimum of 55% of the cost of manufactured products being US-mined, produced, or manufactured), the credit amount jumps to 40% (30% Base + 10% Bonus)5.

A Prepaid PPA provider who uses US-made equipment (e.g., panels from Georgia, racking from Ohio) is potentially receiving a massive 40% subsidy from the government, not just 30%.

Negotiation Insight: If a homeowner is quoted a price for a system using US-made panels, the installer is likely claiming this 10% bonus. The homeowner should push for a lower prepaid price.

- Ask: "Are you claiming the Domestic Content Bonus on this system?"

- If yes: "Then I expect a larger discount on the prepaid amount, as your tax benefit is 33% higher than standard."

This level of detailed questioning signals to the sales representative that the buyer is sophisticated and understands the 2026 tax stack, significantly reducing the likelihood of them offering a predatory or non-compliant contract.

Part V: Counterparty Risk – When Your "Landlord" Goes Bankrupt

In a direct ownership model, if the installer goes bankrupt, the homeowner still owns the panels. They might lose the labor warranty, but the physical asset is theirs. In a Prepaid PPA, the homeowner does not own the panels. They have a contract with a company to use the company's panels. If that company files for Chapter 7 or Chapter 11 bankruptcy, the homeowner is in a precarious legal position.

5.1 The Bankruptcy Estate

Solar panels owned by a bankrupt installer are considered "assets of the estate" under bankruptcy law.

- Scenario A: Reorganization (Chapter 11). The installer (or a new buyer) takes over the contracts. Usually, the service continues, but customer service may degrade. The new owner is generally bound by the terms of the existing PPA.

- Scenario B: Liquidation (Chapter 7). The bankruptcy trustee looks to liquidate assets to pay creditors. While it is unlikely they would pay to remove panels from a roof (as the removal cost often exceeds the resale value of used panels), a state of legal limbo can ensue. The homeowner might be unable to sell their home because the title to the panels is clouded by the bankruptcy proceedings, and the "buyout" option may be frozen.

5.2 Lien Risks and UCC-1 Filings

Since the installer owns the system, their lenders (who provided the capital to buy the panels) may have a UCC-1 financing statement filed against the equipment. This serves as a public notice of their security interest in the panels. While this is a lien on the panels, not the home, aggressive lenders might try to assert that the panels are "fixtures" (part of the real estate) rather than "consumer goods"30.

If the panels are deemed fixtures, the lender's lien could theoretically take priority over subsequent mortgages or complicate a refinance. Recent court rulings, such as In re Evans, have tended to view residential solar systems as consumer goods rather than fixtures, which protects the homeowner's real estate title, but the risk varies by jurisdiction.

Protective Measure: Homeowners should ensure their PPA contract includes a "Non-Disturbance Agreement" acknowledgment. This clause ensures that even if the installer defaults on their loans, their lenders cannot remove the system or disrupt service as long as the homeowner has paid their dues (which they have, via prepayment).

5.3 Transferability and Home Sales

A major friction point for PPAs is the sale of the home. In 2026, most lease and PPA contracts are designed to be transferable. However, the prepaid nature of this specific product simplifies the process significantly. Since there are no remaining monthly payments, the new homebuyer does not need to undergo a credit check to assume the financial obligation—there is no obligation left to assume.

Red Flag: If a Prepaid PPA contract requires a credit check for a home buyer to assume the agreement, this is a sign of a poorly drafted contract or an attempt by the installer to harvest data. The transfer should be administrative only.

Part VI: Regional Context – The State of Solar in 2026

While federal tax policy sets the baseline, state-level incentives and regulations create significant variances in the viability of the Prepaid PPA model.

6.1 California: The Shadow of NEM 3.0

In California, the Net Billing Tariff (NEM 3.0) has drastically reduced the value of exported solar energy. This makes "self-consumption" the primary driver of ROI. For Prepaid PPAs in California, the integration of battery storage is almost mandatory to make the economics work.

The OBBBA's leasing restrictions generally allow for solar PV leasing, but battery storage has its own complex eligibility rules under Section 48E. California homeowners must ensure that if their Prepaid PPA includes a battery, the contract effectively separates the storage element or verifies that the battery independently qualifies for the commercial credit under the "Qualified Energy Storage Technology" definitions. The "Battery Bonus Connect" program and other Virtual Power Plant (VPP) initiatives in California31 offer additional revenue streams that can be stacked on top of the PPA structure, improving the overall value proposition.

6.2 New York: State Credits as a Backstop

New York continues to offer a generous state-level personal tax credit for solar energy systems (25% of cost, capped at $5,000)32. Importantly, this state credit is typically available to the system owner. In a Prepaid PPA, the homeowner is not the owner.

Critical Gap: Homeowners in New York considering a Prepaid PPA must verify if the state credit can be passed through by the installer or if they forfeit this $5,000 benefit by choosing the PPA model. Unlike the federal credit, state credits often have different rules regarding third-party ownership. Losing the $5,000 state credit might negate the benefits of the federal PPA loophole, making a direct purchase (even without the federal 30%) potentially more attractive.

Part VII: Future Outlook & Strategic Recommendations

The era of "easy solar"—sign a paper, get a check from the IRS—is over. The market of 2026 is a market of financial engineering. The "Prepaid PPA" is a legitimate tool to bridge the subsidy gap, effectively allowing homeowners to "buy" the commercial tax credit they are no longer eligible for as individuals. However, this tool is sharp. It requires consumers to navigate IRS regulations, assess corporate bankruptcy risk, and scrutinize supply chains.

The "free lunch" of the $1 buyout is the most dangerous trap in the market; avoiding it requires accepting the slight uncertainty of a "Fair Market Value" transfer. For the homeowner in 2026, the path to solar savings is no longer just about photons and panels; it is about contracts and code sections.

7.1 The Consumer Playbook: A "Red Flag" Checklist

To navigate this complex landscape, homeowners should use the following checklist to evaluate any Prepaid PPA offer:

| Clause/Feature | Green Light | Red Flag (Walk Away) |

|---|---|---|

| Buyout Price (Year 6) | "Fair Market Value" or "Greater of FMV or 15%" | Fixed "$1" or "Free Transfer" (High Audit Risk) |

| Recapture Indemnity | Installer absorbs risk of tax credit denial | Homeowner indemnifies installer for lost tax credits |

| Panel Ownership | Clear TPO title with path to transfer | Ambiguous or "Disguised Sale" language |

| Bankruptcy Protection | Non-Disturbance Clause included | Silent on Installer Default/Bankruptcy |

| FEOC Compliance | Specific Warranty of FEOC Compliance | Silent on Supply Chain/Origin |

| Transferability | Transferable to home buyer with no fees | "Credit Check Required" for new buyer (on prepaid deal?) |

| System Removal | Installer pays removal if PPA ends | Homeowner pays removal costs |

7.2 The "Hybrid" Alternative: Community Solar & VPPs

If the complexity and risk of a Prepaid PPA are too high, homeowners should consider the alternatives that are maturing in 2026:

- Virtual Power Plants (VPPs): Programs like the "Battery Bonus Connect" in California allow homeowners to own a battery and receive payments for grid services. These revenue streams can offset the lack of an ITC and are often compatible with various ownership models33.

- Community Solar: Subscribing to a commercial solar farm allows the homeowner to benefit from solar without the ownership risks. The commercial entity owns the farm, claims the 48E credit, and passes savings to the subscriber. In 2026, this is often the "cleanest" financial choice for risk-averse homeowners who do not want to navigate the disguised sale minefield.

Works cited

- Federal Solar Tax Credit (ITC): Ending January 1, 2026, accessed January 30, 2026, https://www.solartopps.com/blog/federal-solar-tax-credit-ending-january-1-2026/

- How the Federal Solar Tax Credit Works In 2026 - Paradise Energy Solutions, accessed January 30, 2026, https://www.paradisesolarenergy.com/blog/how-does-the-solar-tax-credit-work/

- Expiration and Carryforward Rules for the Residential Clean Energy Credit | Congress.gov, accessed January 30, 2026, https://www.congress.gov/crs-product/IN12611

- What to Know About Expiring Energy Tax Credits - NAHB, accessed January 30, 2026, https://www.nahb.org/blog/2025/07/expiring-energy-tax-credits

- Commercial Solar Tax Credits 2026: Federal Incentives for Businesses, accessed January 30, 2026, https://goodenergysolutions.com/commercial-solar-tax-credits-2026-federal-incentives-for-businesses/

- Prepaid Solar Lease and PPA: A Guide for Homeowners, accessed January 30, 2026, https://www.solarinsure.com/prepaid-solar-lease-ppa-a-guide-for-homeowners

- Prepaid Solar Leases & PPAs: A New Path for Going Solar in 2026, accessed January 30, 2026, https://www.solar.com/learn/prepaid-solar-leases-ppas/

- Residential Clean Energy Credit | Internal Revenue Service, accessed January 30, 2026, https://www.irs.gov/credits-deductions/residential-clean-energy-credit

- Summary of Inflation Reduction Act provisions related to renewable energy | US EPA, accessed January 30, 2026, https://www.epa.gov/green-power-markets/summary-inflation-reduction-act-provisions-related-renewable-energy

- Your 2026 Guide to Commercial Solar Tax Credits - JK Renewables, accessed January 30, 2026, https://www.jkrenewables.com/post/your-2026-guide-to-commercial-solar-tax-credits

- House Bill Accelerates Phaseout of Clean Energy Tax Credits and Restricts Leasing and Transferability | Paul Hastings LLP, accessed January 30, 2026, https://www.paulhastings.com/insights/phast-track-legal-insights-on-environment-energy-and-infrastructure/house-bill-accelerates-phaseout-of-clean-energy-tax-credits-and-restricts-leasing-and-transferability

- 'One Big Beautiful Bill Act' Signed Into Law and Executive Order With Major Impacts on Clean Energy Tax Credits | Paul Hastings LLP, accessed January 30, 2026, https://www.paulhastings.com/insights/client-alerts/one-big-beautiful-bill-act-signed-into-law-and-executive-order-with-impacts-on-clean-energy-on-clean-energy-tax-credits

- The One Big Beautiful Bill Act: Navigating clean energy tax credits in a new era - McDermott Will & Schulte, accessed January 30, 2026, https://www.mwe.com/insights/the-one-big-beautiful-bill-act-navigating-clean-energy-tax-credits-in-a-new-era/

- One Big Beautiful Bill Act to Scale Back Clean Energy Tax Credits Under Inflation Reduction Act | Insights | Holland & Knight, accessed January 30, 2026, https://www.hklaw.com/en/insights/publications/2025/06/senate-moves-to-scale-back-clean-energy-tax-credits-latest-updates

- Project Solar: 6 year prepaid PPA that transfers ownership to you for zero cost - Reddit, accessed January 30, 2026, https://www.reddit.com/r/solar/comments/1m22amc/project_solar_6_year_prepaid_ppa_that_transfers/

- ALLOCATED TAX CREDIT INVESTMENTS - Foss & Company, accessed January 30, 2026, https://fossandco.com/wp-content/uploads/2020/10/FossCo-Tax-Whitepaper-R6.pdf

- Is Prepaid Solar Better than the Original Tax Credit?, accessed January 30, 2026, https://www.solar.com/learn/is-prepaid-solar-better-than-the-original-tax-credit/

- Recognizing When a Disguised Sale of Property Takes Place - The Tax Adviser, accessed January 30, 2026, https://www.thetaxadviser.com/issues/2016/aug/recognizing-disguised-sale-of-property/

- Partnership Disguised Sale Rules and Exception | Cherry Bekaert, accessed January 30, 2026, https://www.cbh.com/insights/articles/partnership-disguised-sale-rules-and-exception/

- 26 CFR § 1.707-3 - Disguised sales of property to partnership; general rules., accessed January 30, 2026, https://www.law.cornell.edu/cfr/text/26/1.707-3

- Solar Purchase Power Agreement Template, accessed January 30, 2026, https://www.purchase.edu/live/files/940-rfp-su-060815-addendum-4-ppa-template

- Attachment 3- Sample Power Purchase Agreement (PPA) - SUNY System Administration, accessed January 30, 2026, https://system.suny.edu/media/suny/content-assets/documents/capital-facilities/ENG-01-Solar-PV-Projects-ATTACHMENT-3-PPA.docx

- tsla-20251231 - SEC.gov, accessed January 30, 2026, https://www.sec.gov/Archives/edgar/data/1318605/000162828026003952/tsla-20251231.htm

- Working Through The FEOC Maze | Norton Rose Fulbright - July 2025, accessed January 30, 2026, https://www.projectfinance.law/publications/2025/july/working-through-the-feoc-maze/

- A Comprehensive Guide to Prohibited Foreign Entities for Clean Energy Tax Credits, accessed January 30, 2026, https://www.reunioninfra.com/insights/comprehensive-guide-to-prohibited-foreign-entities-for-clean-energy-tax-credits

- What Are The Best Solar Panel Brands in 2026?, accessed January 30, 2026, https://empiresolarny.com/best-solar-panel-brands-2026/

- FEOC Compliance Solar Installers: 2026 Checklist For Installers - Energyscape Renewables, accessed January 30, 2026, https://energyscaperenewables.com/post/feoc-compliance-solar-installers-checklist-2026/

- Solar ITC Safe Harbors After the “Big Beautiful Bill”: What Developers Need to Know, accessed January 30, 2026, https://www.greenbaumlaw.com/insights-alerts-Solar-ITC-Safe-Harbors-After-the-Big-Beautiful-Bill-What-Developers-Need-to-Know.html

- Treasury Department Adds Restrictions to Beginning of Construction Rules for Wind and Solar Facilities - Chapman and Cutler LLP, accessed January 30, 2026, https://www.chapman.com/publication-treasury-department-adds-restrictions-to-beginning-of-construction-rules-for-wind-and-solar-facilities

- Court Rules That Financed Residential Solar System Is a Consumer Good, Not a Fixture, accessed January 30, 2026, https://www.bradley.com/insights/publications/2024/03/court-rules-that-financed-residential-solar-system-is-a-consumer-good-not-a-fixture

- No-cost virtual power plant offering for Clean Energy Alliance customers - pv magazine USA, accessed January 30, 2026, https://pv-magazine-usa.com/2025/06/17/no-cost-virtual-power-plant-offering-for-clean-energy-alliance-customers/

- 2026-2027 U.S. Solar and HVAC Incentives After Federal Credits End | AC Direct, accessed January 30, 2026, https://www.acdirect.com/blog/2026-2027-us-solar-hvac-incentives-post-federal-credit-era/

- US virtual power plant programmes advance with new partnerships and investment - Energy-Storage.News, accessed January 30, 2026, https://www.energy-storage.news/us-virtual-power-plant-programmes-advance-with-new-partnerships-and-investment/